Hospitals brace for leaner contracts as Medicare Advantage plans face financial pressures

Changes in MA plans for 2026 also include a shift from PPOs to HMOs.

A rare reduction in Medicare Advantage (MA) enrollment projected for 2026, as well as broad cuts in plan availability, could have negative consequences for hospitals and health systems.

MA plans are projecting a 900,000 drop in MA enrollments in 2026, to 34 million, according to CMS. That would drop MA enrollment from a majority of Medicare enrollments to about 48%. In contrast, CMS said it projects flat enrollment.

A projected decrease, which comes ahead of the Oct. 15 start of open enrollment, would mark the first drop in MA enrollments as a share of Medicare since at least 2007, according to tracking by KFF.

“It’s unlikely to be a one-time blip but rather may become the new normal for the foreseeable future,” Lisa Piercey, MD, MBA, managing partner of Tristela Capital Partners, said about the stalled enrollment growth.

She said that enrollment stagnation was likely driven by MA plans dialing back benefits and their geographic footprint in response to cost pressures.

The number of plans health insurers recently announced for 2026, according to tracking by ATI Advisory, also would decrease in most categories, including:

- 9% in combined MA and Part D plans

- 13% in MA-only plans

- 23% in stand-alone Part D plans

Some smaller categories of special needs plans (SNPs) would increase, such as:

- 42% in C-SNPs

- 15% in D-SNPs

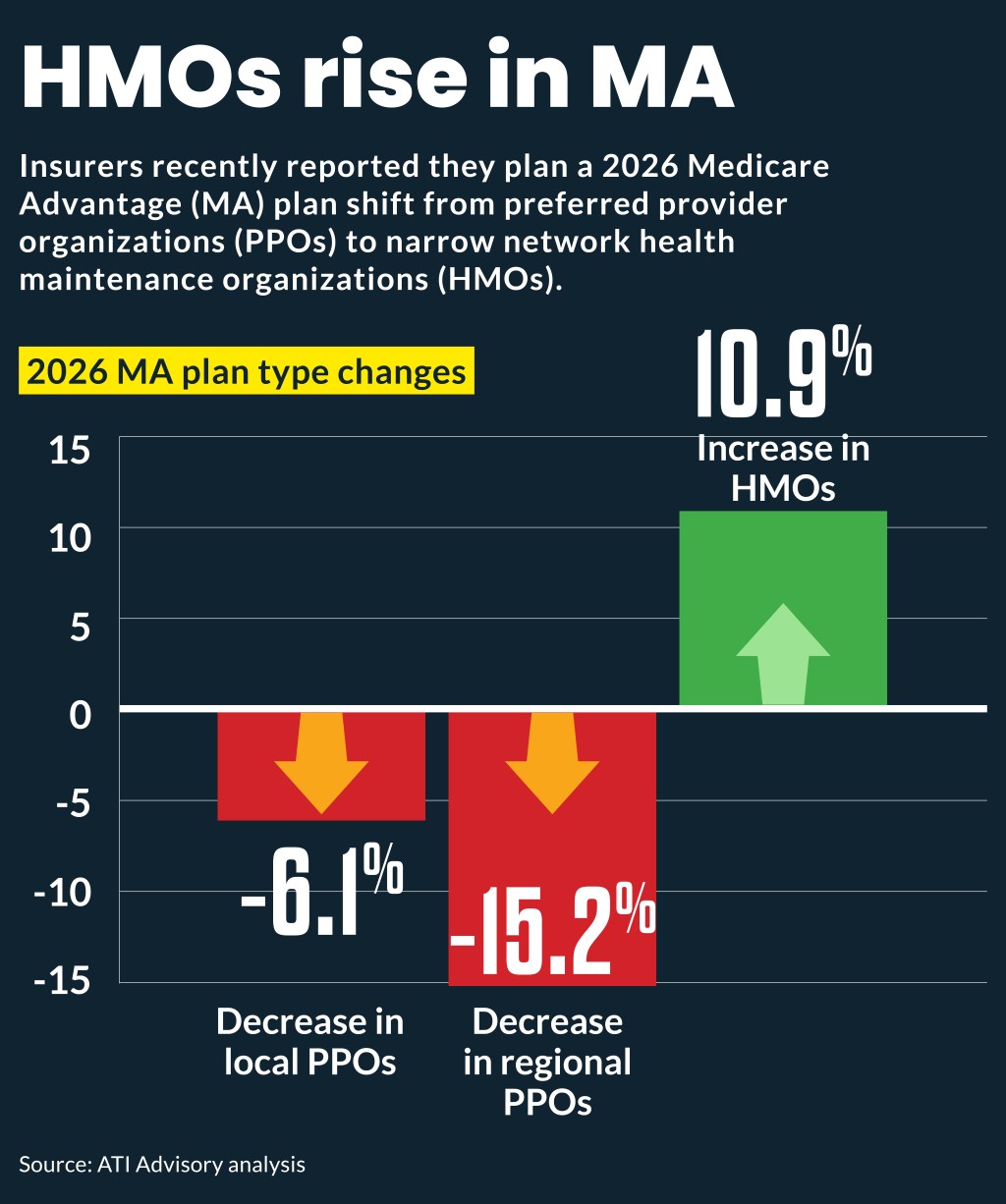

The decrease in larger MA plans was accompanied by a shift in the types of plans offered from preferred provider organizations (PPOs) to narrow network health maintenance organizations (HMOs).

Plan type changes, according to ATI Advisory, include:

- 6.1% decrease in local PPOs

- 15.2% decrease in regional PPOs

- 10.9% increase in HMOs

“PPOs will continue to be an important part of Medicare Advantage, but with the financial and utilization headwinds plans are currently facing, HMOs are better positioned for the moment we are in,” said Allison Rizer, MHS, MBA, chief growth and innovation officer at ATI Advisory.

This trend could reduce some demand and patient panels for out-of-network providers, at least temporarily, Rizer said.

“That said, we’re also seeing increased calls for consumerism and consumer-driven care, meaning PPOs will continue in the long run,” Rizer said.

Driving the changes

Increasing prices and utilization are driving the 2026 changes, said Piercey.

“Instead of chasing enrollment growth at all costs, MA plans are starting to focus on containing spend, driven by rising costs of chronic condition management, specialty pharmacy, and overall higher utilization, layered on top of broader pressures like higher prices from consolidation and added red tape,” said Piercey.

The reduction in plans also comes because “providers are fighting back,” said Brad Gingerich, vice president, revenue cycle operations, payor strategy for Ensemble Health Partners.

“They’re done accepting low payments and bad contract terms,” Gingerich said. “Plus, they’re using rules like the ‘two-midnight rule’ to make sure they get paid fairly, which costs insurers more.”

John Poziemski, a managing director for Kaufman Hall, agreed that pressure has increased from hospitals and health systems, which have become much more selective about which MA plans with which they will contract.

“You have both plans and providers narrowing their focus right now and that’s going to result in some instances in a lot more payer-provider alignment, overall,” Poziemski said. “And there will also be plans and providers on the outside looking in because they aren’t part of the narrow network or this new model that is being shaped.”

Hospital effect

The increasing financial pressures on MA plans directly affect providers.

“Providers should prepare for leaner contracts, and investors will watch closely for models that prove they can bend the cost curve,” Piercey said.

Joyjit Saha Choudhury, a managing director for Kaufman Hall, said the increased financial pressures on MA plans will lead them to push more administrative requirements that can hit providers’ bottom lines.

“All of the prior auth, the denials, the downgrades, other requirements, other clinical programs, new claims edits, those are the things providers need to be more vigilant of,” Choudhury said. “And that needs to work itself into negotiations, into contracts.”

Provider effects from the even-steeper decreases in available Part D plans are most likely to show up in value-based care (VBC) agreements, he said. Drug plan volatility and spiraling costs have led a growing number of providers to tell him they have carved out drug costs from VBC agreements.

Risk appetite

Despite a broad push by MA plans for hospitals and health systems to take on downside risk, those organizations have become more reluctant to do so, said Choudhury.

“The wiser payers are better at working with some of those provider partners to figure out what is the right mutual glide path that’s appropriate for the situation towards risk,” Choudhury said.

Poziemski said downside risk arrangements “are not on pause but slowing down.”

“There was a probably a period in certain markets where the default mode was, ‘Yeah, we’re going to opt into this because there is a lot of money to be made in managing the Medicare population,’” Poziemski said. “And that’s flipped to the default mode being [likely] to opt out of these things.”

Now providers are thinking much more carefully, in advance, about how much risk they want to take on, he said.