Healthcare costs prompt employers to explore alternative health plans

Employers are expecting healthcare median cost increases of as high as 10% in 2026.

Employers are increasingly considering and adopting alternative health plans to counter historic cost increases.

Employers report that they are in the midst of a multi-year surge in healthcare costs and expect those costs to worsen next year.

For example, large employers expect a median 9% increase in healthcare expenses next year, according to recent survey by the Business Group on Health (BGH). They plan to reduce that to a 7.6% increase through various initiatives, which include moving toward alternative health plans.

An even larger 10% median healthcare cost increase was expected by both large and small U.S. businesses recently surveyed of by the International Foundation of Employee Benefit Plans.

“Employers have indicated that cost-sharing, plan design and purchasing/provider initiatives will be the most impactful techniques to manage costs,” Julie Stich, vice president of content at the International Foundation, said in a release.

Alternative plans

Alternative health plans are expected to feature prominently among a variety of planned employer cost-control responses. In 2026, 24% of employers surveyed by BGH will have one of these offerings in place either as an option or a standalone plan. Another 36% are considering this option for 2027 or 2028.

The findings echoed similar projections from a recent Mercer survey, which found 35% of large employers will offer a non-traditional medical plan option in 2026 — up from 6% this year. Those include variable copay plans with no- or low-deductible designs and set copayments for services based on individual providers’ fees. Such copays are fixed and communicated upfront, which allows workers to select lower-cost providers.

The look to alternative health plans come amid increasing employer and employee frustration with high-deductible health plans (HDHPs), which dominate the employer market but leave patients with very large out-of-pocket costs.

Mark Cuban, the high-profile billionaire and co-founder of Cost Plus Drug Co., who has pushed healthcare cost-control initiatives, recently posted on X about HDHPs that “It may sound counter intuitive, but if you can’t afford your deductible, you MIGHT be better off not getting insurance. When you need care, primary, preventive or worse, your doctor or hospital has financing plans. And their cash price that they finance will be cheaper than what your insurance company or employer negotiated.”

Alternative health plans, BGH noted, typically include an element or foundation that sets them distinctly apart from a traditional model. Those can include:

- Targeted provider networks built around free primary care

- No-network reference-based pricing models

- Copay-only plans with strict adherence to evidence-based care via prior authorization

Copay only plans

A McKinsey & Company analysis noted alternative health plans differ from traditional plans by forgoing deductibles or coinsurance, while leaving only a copay that varies by provider. Enrollees are provided simple copays based on the plan’s arrangements with each provider. Those plans can cut employers’ healthcare spend by 6% to 8% annually, McKinsey said.

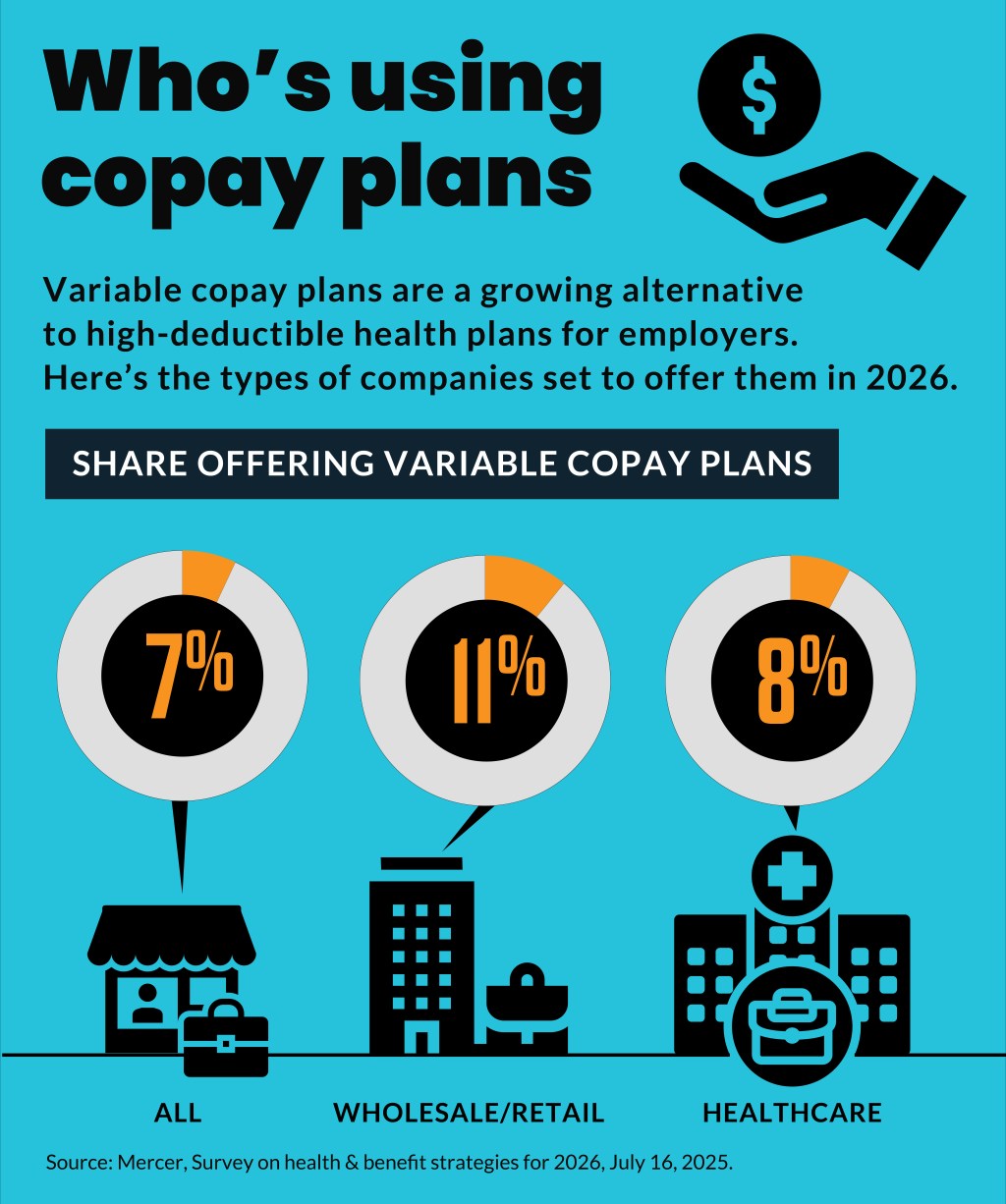

A 2024 Mercer survey found only 7% of employers were already using a copay-only plans or planned to do so in 2025. But another 18% considered such a plan for 2025 or 2026.

A move away from deductibles for patients with employer-sponsored insurance could help providers who have reported increasing financial strain due rising bad debt and charity care from underinsured patients.

A potential downside for providers from such emerging plans is that they could lose volumes if they are placed on a higher copay tier by plans trying to steer enrollees to lower-cost or higher quality providers.

“Tiered, variable-copay plans can benefit hospitals that demonstrate strong outcomes, efficiency, and cost control, aligning well with broader value-based care initiatives,” said Shawn Stack, a policy director for HFMA. “However, these plans may inadvertently disadvantage community hospitals that lack the high-volume purchasing power and advanced technologies larger systems can leverage to better manage costs and drive efficiencies.”

A growing number of commercial payers are offering copay-only plans. For instance, UnitedHealthcare’s Surest plan is the company’s fastest growing commercial plan, according to Alison Richards, CEO of Surest. More than 1 in 4 of the payer’s large customers now offer Surest, up from 1 in 9 in 2023.

Surest uses provider-specific copays but the company said it does not use tiers. Instead, copayments vary based on a “proprietary pricing model” that evaluates historical provider performance and lowers copays for providers evaluated as higher value. That reevaluation — and related changes in copays — is conducted annually.

Employers with 10% plan savings reduce member out-of-pocket costs by an average of 30%, Richards said in a Q&A sent by the company.

High-deductible health plans were intended to push enrollees to shop for services but complexity in determining costs for various services from different providers limited that ability, according to some research.

However, 2020 research on copay plans with tiered networks concluded enrollees would use them to price shop for inpatient care because the “out-of-pocket prices for healthcare are clearly stated, predictable, and simple to understand.”

“Hospitals in high-copay tiers should expect reduced patient volumes,” Elena Prager, the author and now an assistant professor at the Simon Business School at the University of Rochester, wrote in an email. “The magnitude of the reduction can range from negligible to potentially double-digit percent volume losses, depending on a host of factors.”

Reference-based pricing

An increasing number of employers also appear to be offering reference-based pricing (RBP) plans. Mercer’s 2024 survey noted the 2025 expected use of RBP plans — along traditional HMOs and regional health plans — reached 20% of respondents. And another 15% were still considering them for 2025 and 2026.

Savings for employers accelerate to 10% to 30% under RFP, where reimbursement is typically 120% to 170% of Medicare rates, noted McKinsey. McKinsey said that in cases where hospitals do not accept RBP, patients could be responsible for the difference between the provider’s charge and the plan’s allowed amount. In response, RBP payers are launching plans with warranties to cover the member’s cost share if facility negotiations fail.